One of the most important questions multifamily investors ask when exploring CMHC MLI Select financing is simple. How is positive cash flow protected?

The strength of the program lies in its underwriting discipline. CMHC does not rely solely on developer projections or optimistic rent assumptions. Instead, it conducts its own independent financial analysis to determine whether a project can realistically support its debt obligations over the long term.

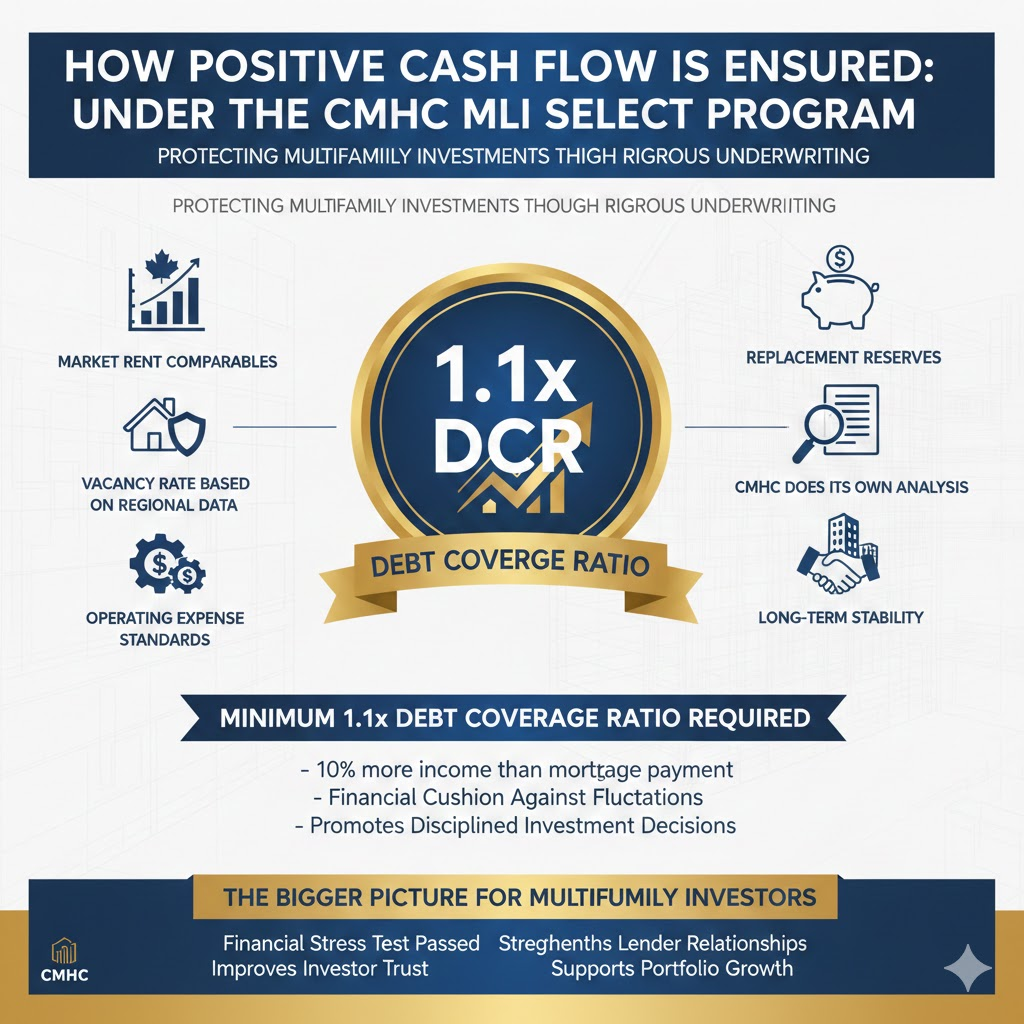

At the center of this evaluation is the debt coverage ratio requirement.

What Is the Debt Coverage Ratio and Why It Matters

The debt coverage ratio, often referred to as DCR, measures a property’s ability to generate enough net operating income to cover its annual debt payments.

Under the CMHC MLI Select Program, a project must demonstrate a projected net operating income equal to at least 110 percent of its projected debt cost. This translates to a minimum 1.1 debt coverage ratio.

In practical terms, this means the building must generate ten percent more income than is required to pay the mortgage. That extra margin acts as a financial cushion.

CMHC Does Its Own Analysis

CMHC does not simply accept a borrower’s rent roll and expense forecast at face value. Instead, it reviews the project using established benchmarks and conservative assumptions.

This includes reviewing

Market rents compared to actual local comparables

Vacancy rates based on regional data

Operating expenses using industry standards

Replacement reserves and maintenance projections

By applying standardized metrics, CMHC reduces the risk of inflated income expectations or underestimated expenses.

Why the 1.1 Requirement Protects Investors

The 1.1 debt coverage ratio requirement serves several important purposes.

First, it ensures the project has breathing room. Even if rents fluctuate slightly or expenses increase, the property should still be able to meet its mortgage payments.

Second, it promotes disciplined acquisition and development decisions. Investors must structure deals that are fundamentally sound, not dependent on aggressive growth projections.

Third, it supports long-term stability. Properties financed under MLI Select are less likely to experience financial stress during market adjustments.

In this way, positive cash flow is not guaranteed by promise. It is supported by rigorous analysis and conservative underwriting.

The Bigger Picture for Multifamily Investors

For investors, this underwriting structure creates confidence. When a project qualifies under MLI Select, it has already passed a financial stress test. That level of review can strengthen lender relationships, improve investor trust, and support portfolio growth.

The minimum 1.1 debt coverage ratio is not a hurdle. It is a safeguard designed to ensure sustainable performance.