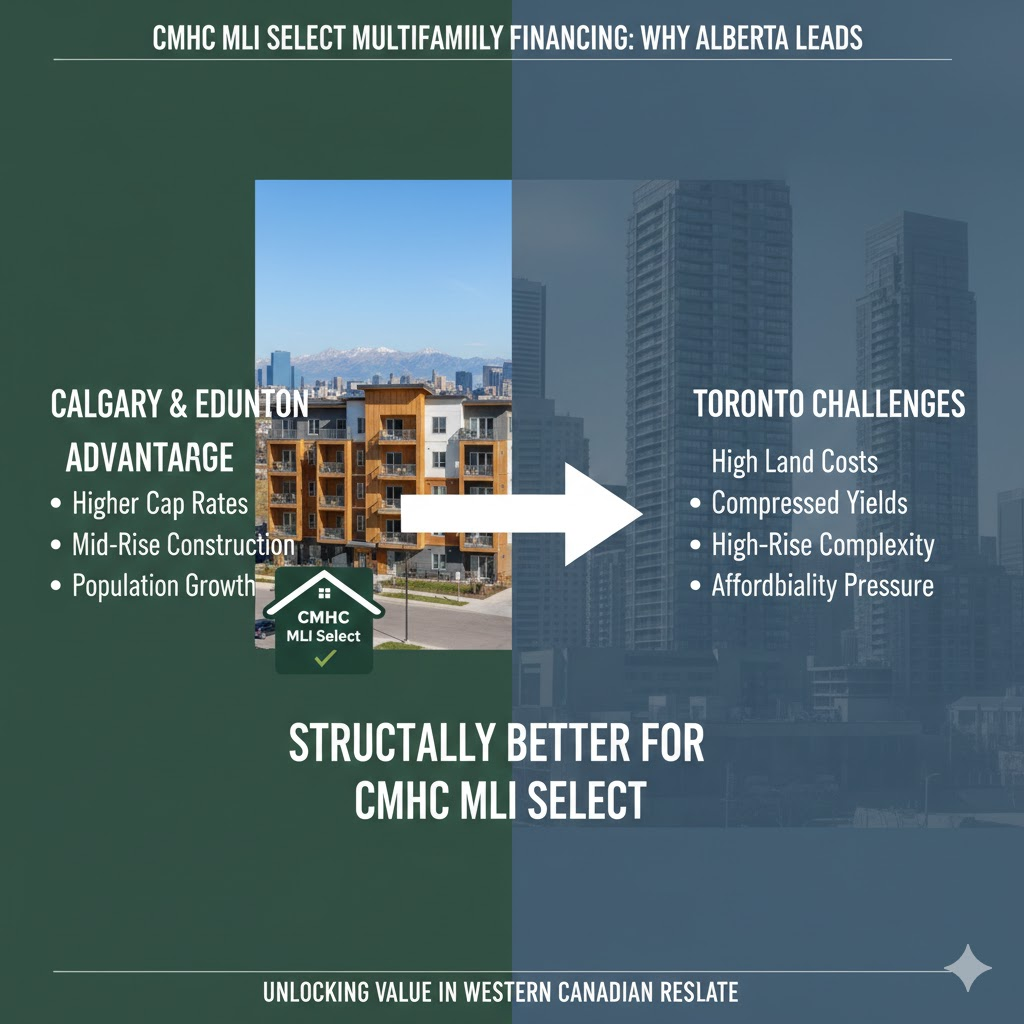

When analyzing Canadian multifamily markets through the lens of CMHC MLI Select financing, it becomes clear that geography plays a decisive role in feasibility. While Toronto dominates national real estate headlines, Calgary and Edmonton often align more naturally with the financial mechanics and policy objectives of performance-based mortgage insurance programs.

This is not about market size. It is about structural compatibility.

To understand why, we must examine five core variables: land economics, yield compression, development feasibility, underwriting alignment, and demographic migration.

1 Land Economics and Capital Stack Pressure

In Toronto, land value often represents a disproportionate percentage of total project cost. Scarcity, urban density, and speculative demand have pushed land acquisition pricing to levels that materially impact financing structure.

High land cost creates three consequences:

First, it compresses the initial yield.

Second, it increases the required equity contribution.

Third, it limits flexibility to integrate affordability components.

CMHC MLI Select rewards affordability and long-term rental commitments. However, when land acquisition already consumes a significant portion of the capital stack, offering below-market rents can materially weaken feasibility unless rents are already extremely high.

In contrast, Calgary and Edmonton operate within more elastic land supply models. While not immune to pricing pressure, both cities provide:

Lower land basis per unit

Greater suburban expansion flexibility

More mid-density development corridors

This reduces capital stack pressure and allows developers to allocate resources toward energy efficiency improvements, accessibility features, and affordability allocations without jeopardizing minimum debt coverage thresholds.

2 Yield Compression and Debt Coverage Alignment

Toronto multifamily assets frequently trade at compressed cap rates due to institutional demand and capital inflows. This compression reduces the spread between net operating income and purchase price.

From an underwriting perspective, this creates tension with CMHC’s minimum 1.1 debt coverage ratio requirement.

Lower initial yield means:

Higher reliance on rent growth projections

Greater sensitivity to interest rate shifts

Reduced margin for underwriting stress tests

Calgary and Edmonton historically demonstrate stronger going-in cap rates relative to acquisition cost. This supports:

More comfortable debt service coverage

Stronger net operating income buffers

Greater resilience under conservative underwriting assumptions

MLI Select underwriting is conservative by design. Markets that naturally produce stronger income to value ratios align more effectively with that framework.

3 Construction Typology and Feasibility

Toronto’s density necessitates high-rise construction in many cases. High-rise development involves:

Longer timelines

Higher material and labor intensity

Greater capital exposure

More complex regulatory approval

These factors increase project risk and delay stabilization timelines.

Calgary and Edmonton feature a broader mix of mid-rise and low-rise multifamily typologies. Wood frame construction over podium, garden-style apartments, and corridor buildings often:

Reduce per-unit construction cost

Shorten build timelines

Simplify project delivery

Lower total capital exposure

This typological difference directly influences financial feasibility when layered with MLI Select criteria.

Energy efficiency upgrades and accessible design integration are often more cost-effective within mid-rise construction models than high-rise concrete towers.

4 Demographic Migration and Rental Demand Stability

Toronto remains a primary immigration gateway. However, affordability pressures have driven substantial interprovincial migration toward Alberta.

Recent migration patterns show:

Net inflows into Calgary and Edmonton

Households seeking a lower cost of living

Professionals relocating for economic opportunity

This migration supports rental absorption without the same speculative pricing pressure found in Toronto.

The result is a more balanced rental ecosystem where:

Demand growth supports occupancy

Acquisition cost remains manageable

Rent levels remain competitive

Balanced markets tend to perform well under structured mortgage insurance models that require sustained operating performance rather than speculative appreciation.

5 Policy Alignment and Program Intent

The CMHC MLI Select Program is structured to incentivize long-term rental stability, affordability, energy performance, and accessibility.

Alberta markets provide:

Development cost structures that support affordability integration

Room for scalable rental supply expansion

Economic diversification supporting stable employment

Toronto remains a strong global market, but its structural economics often prioritize condominium development and capital appreciation strategies over cash flow stability.

MLI Select rewards stable income performance and measurable social outcomes. Calgary and Edmonton frequently present projects that can satisfy both.

Conclusion

The comparative advantage of Edmonton and Calgary over Toronto in the context of CMHC MLI Select is not ideological. It is structural.

Lower land basis, stronger yield profiles, scalable development models, and migration-driven rental demand create an ecosystem where performance-based financing aligns naturally with project economics.

For investors seeking long-term multifamily growth supported by conservative underwriting and enhanced mortgage insurance benefits, Alberta markets often provide a more structurally compatible foundation.