Canada’s housing shortage has intensified across major urban markets, prompting a structural shift in how rental housing is financed. At the center of this shift is the MLI Select program, the federal government’s most powerful financing tool for stimulating multi-unit residential development.

Administered by the Canada Mortgage and Housing Corporation (CMHC), MLI Select is not a grant program. It is a mortgage loan insurance product that enables lenders to offer significantly more favorable financing terms on qualifying multi-family residential properties.

For developers and investors, particularly in high-growth provinces like Alberta, understanding how MLI Select works can dramatically change capital structure, leverage, and long-term returns.

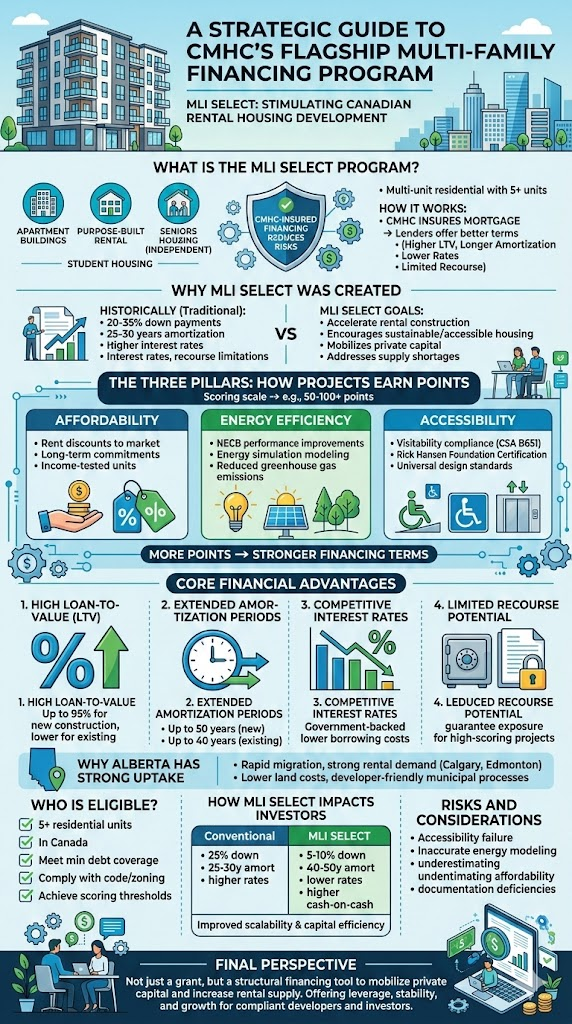

What Is the MLI Select Program?

MLI Select (Multi-Unit Lending Initiative Select) is a CMHC-insured financing program designed for:

- Apartment buildings

- Purpose-built rental housing

- Student housing

- Seniors housing (independent living)

- Multi-unit residential buildings with 5+ self-contained units

Instead of directly lending money, CMHC insures the mortgage. This reduces lender risk, allowing approved financial institutions to offer:

- Higher loan-to-value ratios

- Longer amortization periods

- Lower interest rates

- Potentially limited recourse

The program is performance-based and rewards projects that achieve outcomes in three categories:

- Affordability

- Energy Efficiency

- Accessibility

The more points a project earns across these pillars, the stronger the financing terms.

Why MLI Select Was Created

Traditional commercial lending models were not designed to scale rental housing supply.

Historically:

- Multi-family properties required 20–35% down payments

- Amortizations were capped at 25–30 years

- Interest rates were higher than residential mortgages

- Recourse requirements limited portfolio growth

CMHC recognized that increasing rental supply required structural financing reform, not short-term subsidies.

MLI Select was introduced to:

- Accelerate purpose-built rental construction

- Encourage sustainable and accessible housing

- Mobilize private capital at scale

- Address housing supply shortages nationwide

Core Financial Advantages

1. High Loan-to-Value (LTV)

MLI Select allows financing up to:

- 95% LTV for qualifying new construction

- Lower thresholds for existing properties, depending on the scoring

This significantly reduces the required equity compared to conventional commercial lending.

2. Extended Amortization Periods

The program offers:

- Up to 50 years of amortization for new construction projects, achieving high scores

- Up to 40 years for existing properties

Longer amortization reduces monthly debt service, improving cash flow and debt coverage ratios.

3. Competitive Interest Rates

Because loans are CMHC-insured, lenders treat them similarly to government-backed assets.

This often results in:

- Lower borrowing costs

- Improved rate stability

- Enhanced investor returns

4. Limited Recourse Potential

High-scoring projects may qualify for reduced personal guarantee exposure, enabling investors to scale portfolios without overleveraging personal balance sheets.

The Three Pillars: How Projects Earn Points

MLI Select is a scoring-based system.

Projects earn points across three categories:

1. Affordability

- Rent discounts relative to the market

- Long-term affordability commitments

- Income-tested units

2. Energy Efficiency

- NECB performance improvements

- Energy simulation modeling

- Reduced greenhouse gas emissions

3. Accessibility

- Visitability compliance (CSA B651)

- Rick Hansen Foundation Certification

- Universal design standards

The higher the combined score (e.g., 50 or 100 points), the better the financing incentives.

Why Alberta Has Strong Uptake

MLI Select adoption has been particularly strong in Alberta due to:

- Rapid interprovincial migration

- Strong rental demand in cities like Calgary and Edmonton

- Lower land acquisition costs compared to Toronto or Vancouver

- Developer-friendly municipal processes in certain corridors

The combination of affordable land and high leverage financing creates strong yield potential.

Who Is Eligible?

To qualify, properties must:

- Contain 5+ self-contained residential units

- Be located in Canada

- Meet minimum debt coverage requirements

- Comply with building code and zoning regulations

- Achieve required scoring thresholds

Borrowers must demonstrate:

- Financial capacity

- Development or property management experience

- Stable operating projections

How MLI Select Impacts Investors

For investors, MLI Select changes the math.

Instead of:

- 25% down

- 25-year amortization

- Higher rates

You may access:

- 5–10% down (depending on structure)

- 40–50-year amortization

- Lower rates

- Higher cash-on-cash return

The result: improved scalability and capital efficiency.

Risks and Considerations

MLI Select is powerful, but not automatic.

Common challenges include:

- Failing to meet accessibility baseline (100% visitability)

- Inaccurate energy modeling

- Underestimating affordability commitment timelines

- Documentation deficiencies

Financing approval depends on strict compliance.

Final Perspective

MLI Select is not simply another government housing initiative; it is a structural financing tool designed to mobilize private capital and increase Canada’s rental housing supply.

By combining government-backed mortgage insurance with performance-based incentives, CMHC has created one of the most powerful multi-family financing platforms in the country.

For investors and developers willing to understand its scoring system and compliance requirements, MLI Select offers leverage, stability, and long-term portfolio growth opportunities that conventional commercial lending simply cannot match.

Frequently Asked Questions for CMHC’s Flagship Multi-Family Financing Program

Q.Is MLI Select a grant program?

No. It is a mortgage loan insurance program administered by CMHC.

Q. What types of properties qualify?

Multi-unit residential buildings with five or more self-contained units.

Q. Can small investors use MLI Select?

Yes, provided qualification criteria are met, and the project meets scoring requirements.

Q. Is it only for affordable housing?

No. Market-rate rental projects qualify, though affordability points can enhance financing terms.

Q. How long does approval take?

Timelines vary based on complexity, but proper documentation significantly reduces delays.

Q. Is MLI Select available nationwide?

Yes, but market impact and uptake vary by province.

Tags

Written by Hafil Perincheeri | Connect:LinkedIn | Contact: Email