How CMHC MLI Select Is Transforming Multi-Residential Investing in Canada

Multi-residential real estate in Canada has long been one of the most reliable paths to building generational wealth. Apartment buildings, duplexes, multiplexes, and purpose-built rental developments offer recurring income, inflation protection, and strong long-term appreciation.

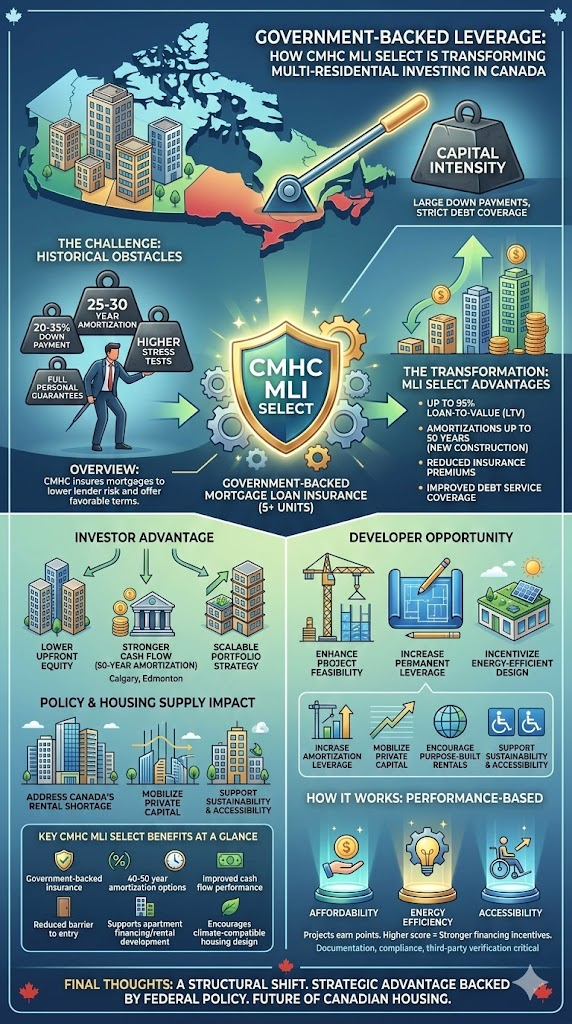

But historically, one obstacle has slowed investor growth:

Capital intensity.

Large down payments, strict debt coverage ratios, and 25–30 year amortizations have made scaling multi-family portfolios difficult even for experienced investors.

That changed with the introduction of the Canada Mortgage and Housing Corporation (CMHC) MLI Select program.

Today, MLI Select financing is one of the most powerful tools reshaping multi-residential investing, apartment financing, and rental property development in Canada.

Overview: What Is CMHC MLI Select?

MLI Select (Multi-Unit Lending Initiative Select) is a government-backed mortgage loan insurance program designed for multi-unit residential properties with five or more self-contained units.

Rather than lending directly, CMHC insures the mortgage. This lowers lender risk and allows approved financial institutions to offer:

- Higher loan-to-value ratios

- Extended amortization periods

- Competitive interest rates

- Potential limited recourse options

The program rewards projects that align with national priorities, including:

- Rental housing supply

- Energy efficiency

- Accessibility

- Affordability

For investors, this translates into enhanced leverage and improved cash flow compared to traditional commercial financing.

What Makes MLI Select Different From Traditional Multi-Family Financing?

Conventional apartment building loans typically require:

- 20–35% down payment

- 25–30 year amortization

- Higher stress-tested debt service ratios

- Full personal guarantees

MLI Select financing restructures that model.

Qualified projects may access:

- Up to 95% loan-to-value (LTV)

- Amortizations up to 50 years (new construction)

- Reduced insurance premiums

- Improved debt service coverage

This fundamentally changes how investors approach multi-residential development and acquisition.

Perspective 1: The Investor Advantage

For real estate investors, the biggest benefits are leverage and scalability.

1. Lower Upfront Equity

With up to 95% LTV, investors can:

- Preserve working capital

- Acquire larger assets

- Diversify across multiple properties

- Maintain liquidity for renovations or reserves

Instead of concentrating capital in one building, investors can scale strategically.

2. Stronger Cash Flow Through 50-Year Amortization

Extended amortization reduces monthly debt payments.

This improves:

- Net operating income (NOI) stability

- Debt service coverage ratios

- Cash-on-cash returns

- Long-term portfolio resilience

Lower payments provide a cushion during economic shifts or vacancy fluctuations.

3. A Scalable Portfolio Strategy

MLI Select is not just financing; it is a growth strategy.

By lowering equity requirements and stabilizing cash flow, investors can:

- Build larger multi-family portfolios

- Develop purpose-built rentals

- Reinvest capital into additional acquisitions

- Structure long-term wealth creation more efficiently

In fast-growing provinces like Alberta, particularly in cities such as Calgary and Edmonton, this leverage can create a competitive advantage in supply-constrained rental markets.

Perspective 2: The Developer Opportunity

For developers, MLI Select enhances project feasibility.

Construction financing often struggles with:

- Rising material costs

- Land acquisition pressures

- Interest rate sensitivity

- Long stabilization timelines

MLI Select improves feasibility by:

- Increasing permanent financing leverage

- Extending amortization for stabilized assets

- Incentivizing energy-efficient and accessible design

Projects aligned with MLI Select scoring criteria can unlock higher returns while meeting federal housing objectives.

Perspective 3: The Policy & Housing Supply Impact

From a national standpoint, MLI Select addresses Canada’s rental housing shortage.

Rather than direct subsidies, the program:

- Mobilizes private capital

- Encourages purpose-built rental development

- Supports long-term housing sustainability

- Incentivizes accessible and energy-efficient construction

This creates alignment between public policy and private investment returns.

Key CMHC MLI Select Benefits at a Glance

- Government-backed mortgage insurance

- Up to 95% LTV financing

- 40–50 year amortization options

- Improved cash flow performance

- Reduced barrier to entry for multi-unit investing

- Supports apartment building financing and rental development

- Encourages climate-compatible housing design

Important Considerations

MLI Select is performance-based.

Projects must earn points across three categories:

- Affordability

- Energy Efficiency

- Accessibility

The higher the score, the stronger the financing incentives.

Documentation, compliance, and third-party verification are critical for approval.

Final Thoughts: A Structural Shift in Multi-Residential Investing

The CMHC MLI Select program represents a structural shift in how multi-family real estate is financed in Canada.

It reduces capital barriers, strengthens long-term cash flow, and enables investors to scale portfolios in ways traditional commercial lending often cannot support.

For investors focused on multi-residential investing, apartment building financing, and rental property portfolio growth, MLI Select is more than a financing product; it is a strategic advantage backed by federal policy and designed for the future of Canadian housing.

Frequently Asked Questions for Transforming Multi-Residential Investing in Canada

Q. What types of properties qualify for CMHC MLI Select?

Multi-unit residential buildings with five or more self-contained units, including apartment buildings and purpose-built rentals.

Q. Is MLI Select only for affordable housing?

No. Market-rate rental projects can qualify, though affordability components can increase point totals.

Q. How much down payment is required?

Qualified projects may access financing up to 95% LTV, significantly reducing required equity compared to conventional commercial loans.

Q. What is the maximum amortization?

Up to 50 years for new construction and up to 40 years for existing properties, depending on scoring.

Q. Does MLI Select improve cash flow?

Yes. Extended amortization lowers monthly debt payments, improving long-term financial performance.

Q. Is it available across Canada?

Yes. The program operates nationwide, though uptake and market impact vary by region.

Tags

Written by Hafil Perincheeri | Connect: LinkedIn | Contact: Email