A Strategic Breakdown of Requirements and Scoring Mechanics

Securing enhanced financing under the Canada Mortgage and Housing Corporation MLI Select program is not accidental.

The program is built on a clear principle: financially sound, socially responsible, and environmentally sustainable multi-residential projects deserve stronger mortgage terms.

For developers and investors across Canada, particularly in growth markets like Alberta, understanding how CMHC evaluates risk and assigns MLI Select points can significantly improve approval odds and unlock better leverage.

This guide provides a strategic breakdown of MLI Select requirements, underwriting mechanics, and scoring optimization techniques.

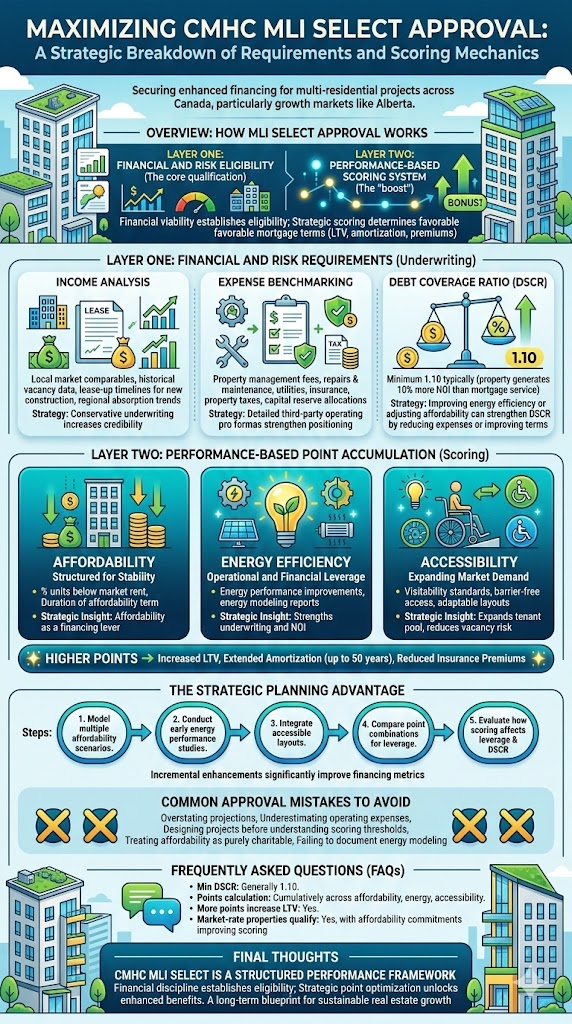

Overview: How CMHC MLI Select Approval Works

MLI Select approval operates on a two-layer qualification framework:

- Financial and Risk Eligibility

- Performance-Based Scoring System

Both layers must be satisfied.

Financial viability establishes eligibility.

Strategic scoring determines how favorable the mortgage terms will be, including loan-to-value ratios, amortization length, and insurance premiums.

Layer One: Financial and Risk Requirements

Before scoring benefits apply, CMHC conducts conservative underwriting to ensure long-term mortgage stability.

1. Income Analysis

Projected rental income is stress-tested against:

- Local market comparables

- Historical vacancy data

- Lease-up timelines for new construction

- Regional absorption trends

If projected rents exceed realistic market conditions, CMHC adjusts them downward. Inflated projections weaken approval probability.

Strategic insight: Conservative underwriting that aligns closely with verified market data increases credibility and speeds review.

2. Expense Benchmarking

Operating expenses are carefully reviewed to prevent unrealistic projections.

CMHC evaluates:

- Property management fees

- Repairs and maintenance

- Utilities

- Insurance

- Property taxes

- Capital reserve allocations

Industry-standard ratios are applied where necessary. Underestimating expenses can reduce approved loan amounts.

Strategic insight: Detailed third-party operating pro formas strengthen financial positioning.

3. Debt Coverage Ratio Requirement

The minimum Debt Service Coverage Ratio (DSCR) is typically 1.10.

This means the property must generate at least 10 percent more net operating income than required to service the mortgage.

Projects operating on thin margins often struggle to qualify.

Strategic insight: Improving energy efficiency or adjusting affordability structures can strengthen DSCR by reducing expenses or improving financing terms.

Layer Two: Performance-Based Point Accumulation

Once financial eligibility is confirmed, borrowers can enhance mortgage terms through strategic point scoring.

MLI Select evaluates projects across three performance categories:

- Affordability

- Energy Efficiency

- Accessibility

Higher points can translate into:

- Increased loan-to-value

- Extended amortization (up to 50 years for new construction)

- Reduced insurance premiums

Affordability: Structured for Stability

Affordability commitments are rewarded based on:

- Percentage of units below market rent

- Duration of affordability term

The greater the commitment, the higher the score.

However, strategic structuring is critical.

Longer amortization and higher leverage often offset reduced rental income, maintaining stable cash flow while increasing total return on equity.

Perspective: For long-term investors, affordability is not a sacrifice, it is a financing lever.

Energy Efficiency: Operational and Financial Leverage

Energy performance improvements serve two purposes:

- Earn MLI Select points

- Reduce long-term operating expenses

Projects that demonstrate measurable reductions in energy consumption, often through energy modeling reports, can reach higher scoring tiers.

Examples include:

- High-performance building envelopes

- Efficient HVAC systems

- Improved insulation standards

- Advanced energy modeling documentation

Perspective: Energy efficiency strengthens both underwriting and long-term net operating income.

Accessibility: Expanding Market Demand

Accessible and adaptable housing design increases inclusivity and long-term tenant appeal.

Scoring may consider:

- Visitability standards

- Barrier-free access

- Adaptable unit layouts

As demographic trends shift toward aging populations and inclusive design expectations, accessible multi-family housing becomes both a social asset and a market advantage.

Perspective: Accessibility is not merely compliance, it expands tenant pools and reduces vacancy risk.

The Strategic Planning Advantage

The strongest MLI Select applications are structured early, often during land acquisition or conceptual design.

Strategic investors typically:

- Model multiple affordability scenarios

- Conduct early energy performance studies

- Integrate accessible layouts into architectural plans

- Compare point combinations to financing improvements

- Evaluate how scoring changes affect leverage and DSCR

Often, incremental design enhancements can significantly improve financing metrics.

For example, a modest energy performance upgrade may unlock higher amortization, which in turn improves overall project feasibility.

Common Approval Mistakes to Avoid

- Overstating rental projections

- Underestimating operating expenses

- Designing projects before understanding scoring thresholds

- Treating affordability as purely charitable rather than strategic

- Failing to document energy modeling properly

MLI Select rewards preparation, not improvisation.

Final Thoughts

The CMHC MLI Select program is not just a financing option, it is a structured performance framework.

Financial discipline establishes eligibility.

Strategic point optimization unlocks enhanced benefits.

For multi-family investors focused on multi-residential financing, apartment development, and scalable rental portfolios in Canada, understanding the scoring mechanics is essential.

With deliberate planning and disciplined underwriting, MLI Select becomes more than mortgage insurance.

It becomes a long-term blueprint for sustainable real estate growth.

Frequently Asked Questions for Maximizing CMHC MLI Select Approval

Q. What is the minimum debt coverage ratio for MLI Select?

Generally 1.10, meaning the property must generate at least 10 percent more income than required to service the mortgage.

Q. How are MLI Select points calculated?

Points are earned across affordability, energy efficiency, and accessibility categories. Higher cumulative scores unlock stronger mortgage terms.

Q. Does earning more points increase the loan-to-value?

Yes. Higher scores may allow increased leverage and longer amortization periods.

Q. Can market-rate properties qualify?

Yes. Market-rate multi-residential projects may qualify, though affordability commitments can significantly improve scoring.

Q. Is energy modeling mandatory?

To earn higher energy efficiency points, formal documentation such as energy modeling reports is required.

Q. When should investors plan for MLI Select?

Ideally, during acquisition or early design stages. Retrofitting for points after planning is less efficient and more costly.

Tags

Written by Hafil Perincheeri | Connect: Linkedin | Contact: Email