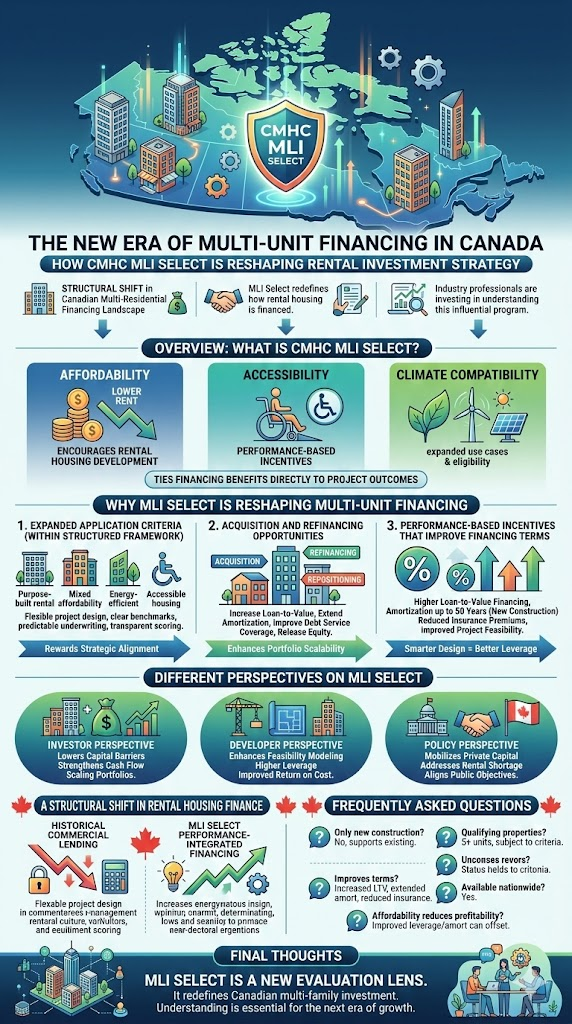

How CMHC MLI Select Is Reshaping Rental Investment Strategy

The Canadian multi-residential financing landscape is undergoing a structural shift.

Since its launch, the Canada Mortgage and Housing Corporation’s MLI Select program has become one of the most influential developments in multi-unit mortgage financing, apartment building investment, and rental housing development across Canada.

Investors, developers, and asset managers are paying attention for one simple reason:

MLI Select does not merely insure mortgages.

It redefines how rental housing is financed.

Understanding its impact requires more than reviewing program guidelines. Industry professionals across Canada have invested time in seminars, direct consultations, underwriting analysis, and strategic modeling to fully understand how this framework influences acquisition strategy, refinancing decisions, and feasibility for new construction.

The conclusion is clear.

MLI Select represents a structural evolution in Canadian multi-unit lending.

Overview: What Is CMHC MLI Select?

MLI Select is a government-backed insured mortgage program designed to encourage the development and preservation of rental housing aligned with three national priorities:

- Affordability

- Accessibility

- Climate compatibility

While it builds upon earlier CMHC programs, MLI Select introduces expanded eligibility, broader use cases, and performance-based incentives that significantly enhance its impact.

Unlike traditional commercial lending, MLI Select ties financing benefits directly to project outcomes. The stronger a project aligns with federal housing priorities, the more favorable the financing terms may become.

This transforms financing into a strategic lever rather than a simple capital tool.

Why MLI Select Is Reshaping Multi-Unit Financing

Industry leaders identify three major shifts that make MLI Select transformative.

1. Expanded Application Criteria Within a Structured Framework

One of the most important changes under MLI Select is its broader application scope.

The program accommodates:

- Purpose-built rental developments

- Mixed affordability projects

- Energy-efficient buildings

- Accessible housing initiatives

- Market-rate rental properties with qualifying performance metrics

At the same time, CMHC has introduced a more structured and performance-based review process.

For investors, this means:

- Greater flexibility in project design

- Clear performance benchmarks

- Predictable underwriting expectations

- Transparent scoring mechanics

Rather than restricting project types, MLI Select rewards strategic alignment.

2. Acquisition and Refinancing Opportunities

Unlike many housing programs that focus solely on new construction, MLI Select supports:

- Acquisition of existing multi-unit properties

- Refinancing of stabilized rental assets

- Capital repositioning strategies

This is a fundamental shift in multi-family mortgage strategy.

Owners of stabilized apartment buildings can refinance under MLI Select to:

- Increase loan-to-value ratios

- Extend amortization periods

- Improve debt service coverage

- Release equity for portfolio expansion

This creates capital recycling opportunities that were previously difficult under conventional commercial financing.

For long-term investors, this enhances portfolio scalability.

3. Performance-Based Incentives That Improve Financing Terms

The most compelling element of MLI Select is its incentive structure.

Projects that score higher across affordability, energy efficiency, and accessibility may qualify for:

- Higher loan-to-value financing

- Amortization periods up to 50 years for new construction

- Reduced mortgage insurance premiums

- Improved overall project feasibility

This performance-based approach shifts investor thinking.

Instead of viewing affordability or energy standards as constraints, they become financing advantages.

In practical terms, smarter design decisions can directly improve leverage and long-term cash flow.

Different Perspectives on MLI Select

The Investor Perspective

For private investors, MLI Select lowers capital barriers and strengthens cash flow sustainability. It allows scaling multi-residential portfolios with improved leverage and longer-term financial stability.

The Developer Perspective

For builders, the program enhances feasibility modeling. Extended amortization and higher leverage can offset construction cost pressures and improve cost-return projections.

The Policy Perspective

From a housing supply standpoint, MLI Select mobilizes private capital to address Canada’s rental shortage. Instead of direct subsidies, it uses mortgage insurance incentives to align public objectives with private returns.

A Structural Shift in Rental Housing Finance

Historically, multi-unit commercial mortgages in Canada relied on:

- Conservative loan-to-value ratios

- Shorter amortization periods

- Strict stress-tested underwriting

- Limited flexibility for refinancing

MLI Select introduces a framework where financing improves when projects demonstrate measurable social and environmental alignment.

This marks a clear departure from purely risk-based lending toward performance-integrated financing.

Final Thoughts: Preparing for the New Standard

CMHC MLI Select is more than a mortgage insurance product.

It introduces a new evaluation lens for multi-unit real estate investment in Canada. Broader eligibility, refinancing flexibility, and performance-based incentives collectively position it as a defining force in multi-residential financing strategy.

For investors, developers, and rental housing operators, understanding MLI Select is no longer optional.

It is essential for navigating and capitalizing on the next era of Canadian multi-family investment.

Frequently Asked Questions for Multi-Unit Financing in Canada

Q. Is MLI Select only for new construction?

No. The program supports both new development and the acquisition or refinancing of existing stabilized rental properties.

Q. What types of properties qualify?

Multi-unit residential properties with five or more self-contained units may qualify, subject to financial and performance-based criteria.

Q. How does MLI Select improve loan terms?

Higher-scoring projects may access increased loan-to-value ratios, extended amortization periods, and reduced insurance costs.

Q. Is the program available across Canada?

Yes. MLI Select operates nationwide, though market dynamics vary by region.

Does affordability reduce profitability?

Not necessarily. Improved leverage and longer amortization can offset rental adjustments while strengthening overall financial sustainability.

Tags

Written by Hafil Perincheeri | Connect:Linkedin | Contact: mailhafil@gmail.com