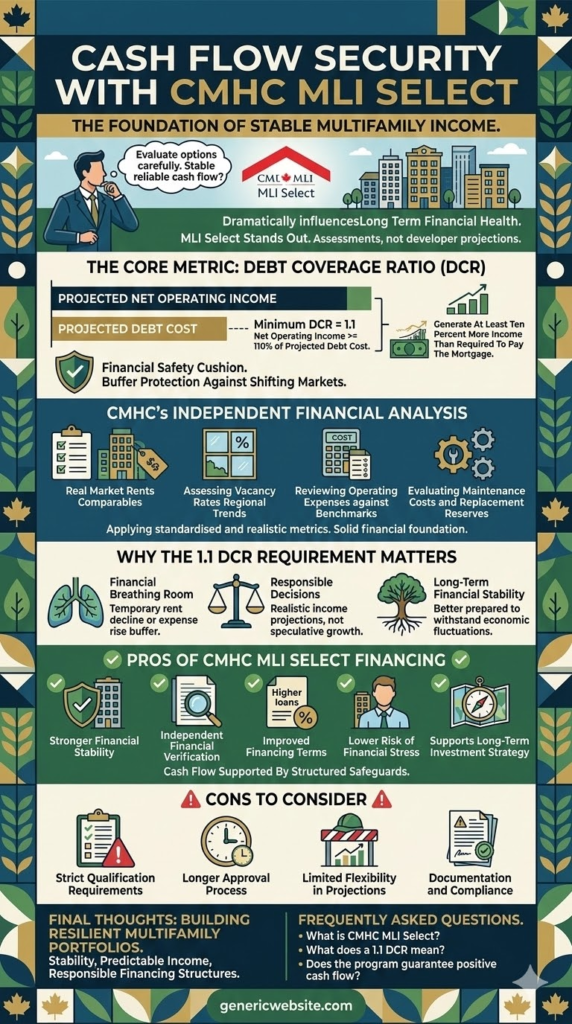

For multifamily investors, one of the most critical questions when evaluating financing options is whether the investment will generate stable and reliable cash flow. Financing structures can dramatically influence a property’s long term financial health, and this is where the CMHC MLI Select Program stands out.

Designed and administered by Canada Mortgage and Housing Corporation, the program emphasizes disciplined financial evaluation. Rather than relying entirely on developer projections, CMHC conducts independent financial assessments to determine whether a property can realistically sustain its mortgage obligations.

At the heart of this process is a key financial metric known as the debt coverage ratio.

Understanding the Debt Coverage Ratio

The debt coverage ratio, commonly referred to as DCR, measures a property’s ability to generate enough income to cover its annual debt payments.

Under the MLI Select framework, a project must demonstrate that its projected net operating income is at least 110 percent of its projected debt cost. This requirement translates to a minimum DCR of 1.1.

In simple terms, the property must generate at least ten percent more income than what is required to pay the mortgage. That additional margin acts as a financial safety cushion.

For investors, this buffer helps ensure that even if market conditions shift slightly, the property can still meet its financial obligations.

Independent Financial Analysis by CMHC

A major reason the program supports stable cash flow is that CMHC performs its own underwriting analysis rather than relying solely on investor estimates.

During this process, CMHC evaluates several financial factors using conservative assumptions and market data. This review includes

- Comparing projected rents with real market comparables

- Assessing vacancy rates based on regional trends

- Reviewing operating expenses against industry benchmarks

- Evaluating maintenance costs and replacement reserves

By applying standardized and realistic metrics, CMHC reduces the risk of overly optimistic projections. This disciplined approach helps ensure that projects entering the program have a solid financial foundation.

Why the 1.1 DCR Requirement Matters

The minimum 1.1 debt-to-coverage ratio is not merely a technical requirement. It plays a significant role in protecting both investors and lenders.

First, it provides financial breathing room. If rents temporarily decline or operating expenses increase, the property still has the capacity to meet its debt payments.

Second, it encourages responsible investment decisions. Developers and property owners must structure deals based on realistic income projections rather than speculative growth.

Third, it promotes long term financial stability. Properties financed under this framework are generally better prepared to withstand economic fluctuations.

This means that positive cash flow is not assumed based on projections alone. Structured financial safeguards support it.

The Bigger Picture for Multifamily Investors

For investors building or expanding multifamily portfolios, the underwriting discipline behind MLI Select creates an added layer of confidence.

When a project qualifies for the program, it has already undergone a rigorous financial stress test. This level of review can strengthen relationships with lenders, improve investor confidence, and support long term portfolio growth.

Combined with benefits such as longer amortization periods and competitive financing structures, the program helps create conditions that support sustainable property performance.

Pros of CMHC MLI Select Financing

Stronger Financial Stability

The 1.1 debt coverage ratio ensures properties maintain a financial cushion against market changes.

Independent Financial Verification

CMHC evaluates market rents, expenses, and vacancy rates using conservative benchmarks.

Improved Financing Terms

Investors may benefit from higher loan to value ratios and longer amortization periods.

Lower Risk of Financial Stress

Careful underwriting helps ensure projects are financially sustainable before approval.

Supports Long Term Investment Strategy

Projects designed under this framework are often more resilient during economic fluctuations.

Potential Cons to Consider

Strict Qualification Requirements

Projects must meet detailed financial and design standards to qualify.

Longer Approval Process

Because CMHC performs its own analysis, approvals may take longer than conventional financing.

Limited Flexibility in Projections

Conservative assumptions may limit overly optimistic revenue projections.

Documentation and Compliance

Developers must provide detailed financial information and maintain program compliance.

Final Thoughts

Positive cash flow is one of the most important factors in successful multifamily real estate investment. The CMHC MLI Select Program helps protect that cash flow through disciplined underwriting and conservative financial standards.

By requiring a minimum 1.1 debt coverage ratio and conducting independent financial analysis, CMHC ensures that projects entering the program are positioned for sustainable long term performance.

For investors seeking stability, predictable income, and responsible financing structures, MLI Select provides a strong foundation for building resilient multifamily portfolios.

Frequently Asked Questions for Cash Flow Security

Q. What is the CMHC MLI Select Program?

The CMHC MLI Select Program is a financing initiative created by Canada Mortgage and Housing Corporation to support multifamily rental housing that prioritizes affordability, sustainability, and accessibility.

Q. What does a 1.1 debt coverage ratio mean?

It means the property must generate at least ten percent more income than its annual mortgage payments, providing a safety margin for financial stability.

Q. Why does CMHC conduct its own financial review?

CMHC performs independent analysis to ensure rental income projections, operating expenses, and vacancy assumptions reflect real market conditions.

Q. Does the program guarantee positive cash flow?

No financing program can guarantee profits, but the underwriting standards significantly improve the likelihood of sustainable cash flow.

Q. Is CMHC MLI Select better than conventional multifamily financing?

For many investors, it can be beneficial because it offers improved loan structures and encourages financially stable projects.

Q. Who typically uses the MLI Select Program?

Real estate developers, multifamily property investors, and housing providers who want long term financing for rental housing projects often use the program.