A Clear Guide to the Financial Criteria for Multi-Family Investment Success

Keywords: CMHC MLI Select requirements, CMHC multifamily financing Canada, multi family investment Canada, apartment building financing, CMHC insured mortgage criteria, multifamily investment strategy, CMHC MLI Select investors

Overview

Multi-family real estate continues to gain attention across Canada as investors search for stable, income-producing assets supported by strong housing demand.

One financing structure that has significantly influenced this sector is the MLI Select program, offered through Canada Mortgage and Housing Corporation.

The program provides mortgage insurance for multi-unit residential properties with five or more units, allowing investors to access enhanced financing terms such as higher loan-to-value ratios, longer amortizations, and improved debt servicing flexibility.

However, these advantages come with clearly defined investor qualifications. Understanding the CMHC MLI Select investor criteria is essential before pursuing a project.

This guide explores the key financial benchmarks investors must meet, explains why they exist, and highlights how they support sustainable multi-family investment across Canada.

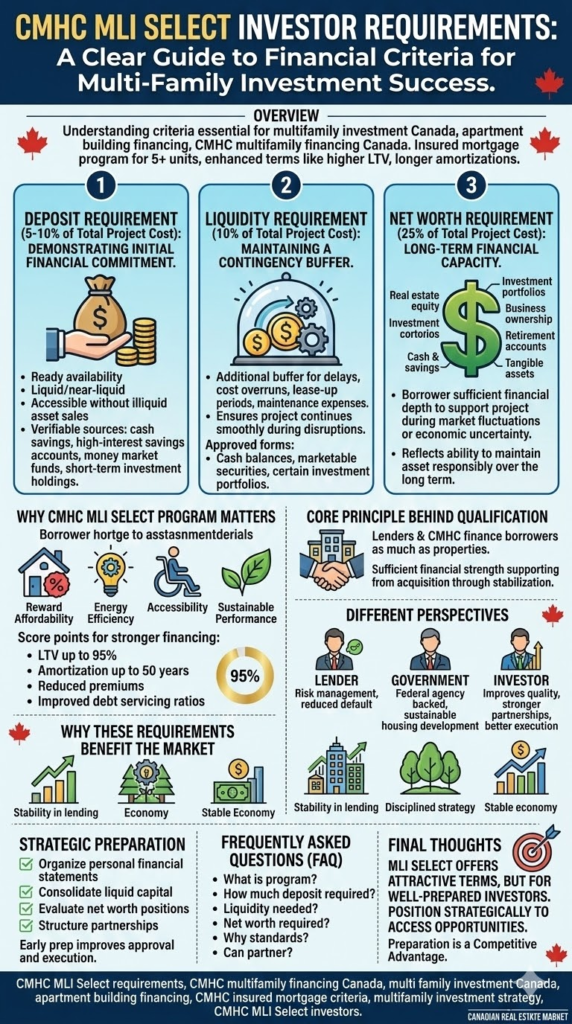

Why the CMHC MLI Select Program Matters for Investors

The MLI Select program was designed to support both housing supply growth and investor participation in the multi-residential market.

Unlike traditional financing models, MLI Select rewards projects that incorporate:

- Affordable rental housing

- Energy-efficient construction

- Accessible housing design

- Sustainable building performance

Projects are evaluated using a points-based scoring system. Higher scoring developments may qualify for stronger financing benefits, such as:

- Loan-to-value ratios up to 95 percent

- Amortization periods up to 50 years

- Reduced mortgage insurance premiums

- Improved debt servicing ratios

These incentives make the program particularly attractive for investors focused on long-term rental housing development and apartment building acquisition.

The Core Principle Behind Investor Qualification

While MLI Select focuses on building housing, lenders and CMHC ultimately finance borrowers as much as properties.

That means investors must demonstrate sufficient financial strength to support a project from acquisition through stabilization and long-term ownership.

Three primary financial benchmarks determine eligibility:

1 Deposit availability

2 Liquidity reserves

3 Net worth strength

Together, these metrics ensure projects are supported by responsible capital and experienced ownership.

1. Deposit Requirement

Demonstrating Initial Financial Commitment

The first requirement for CMHC MLI Select investors is a readily available deposit equal to approximately 5 to 10 percent of the total project cost.

This deposit must meet several criteria.

It must be:

- Liquid or near-liquid

- Accessible without selling illiquid long-term assets

- Verifiable through financial documentation, such as bank or brokerage statements

Acceptable sources often include:

- Cash savings

- High-interest savings accounts

- Money market funds

- Short-term investment holdings

The purpose of the deposit is simple. It demonstrates financial commitment and alignment between the investor, lender, and project outcome.

2. Liquidity Requirement

Maintaining a 10 Percent Contingency Buffer

Beyond the initial deposit, CMHC requires investors to maintain additional liquidity equal to roughly 10 percent of the total project cost.

This reserve acts as a financial safety buffer.

Real estate development and multi-family operations can encounter unexpected challenges, such as:

- Construction delays

- Cost overruns

- Lease-up periods after completion

- Operational or maintenance expenses

By maintaining accessible liquidity, investors can ensure the project continues to operate smoothly even during temporary disruptions.

Common forms of approved liquid assets include:

- Cash balances

- Marketable securities

- Certain investment portfolios approved by lenders

This requirement reinforces financial stability throughout the project lifecycle.

3. Net Worth Requirement

Long-Term Financial Capacity

The third and often most significant requirement is net worth strength.

CMHC typically expects investors to demonstrate a minimum net worth equal to approximately 25 percent of the total project cost.

Net worth calculations may include:

- Real estate equity holdings

- Investment portfolios

- Business ownership value

- Retirement accounts

- Cash and savings

- Other tangible assets

This requirement ensures the borrower has sufficient financial depth to support the project during market fluctuations or economic uncertainty.

From a lending perspective, strong net worth reflects the investor’s ability to maintain the asset responsibly over the long term.

Different Perspectives on the Qualification Standards

Understanding these requirements becomes easier when viewed from multiple perspectives.

The Lender Perspective

Lenders prioritize risk management. Strong investor financials reduce default risk and protect the insured mortgage structure.

The Government Perspective

Because the mortgage insurance program is backed by a federal housing agency, responsible underwriting ensures public resources support sustainable housing development.

The Investor Perspective

While the requirements may appear strict, they actually improve investment quality by ensuring projects are supported by well-capitalized ownership groups.

This often results in stronger partnerships, better execution, and more stable long-term outcomes.

Why These Requirements Benefit the Market

The financial benchmarks within the MLI Select program serve several broader goals.

They help:

- Maintain stability in the multi-family lending market

- Encourage disciplined investment strategies

- Reduce project failure risk

- Support long-term housing supply growth

In many ways, these standards create a healthier investment environment by filtering out undercapitalized projects.

Strategic Preparation for Investors

Investors interested in CMHC MLI Select opportunities often benefit from early financial preparation.

This may include:

- Organizing personal financial statements

- Consolidating liquid capital

- Evaluating net worth positions

- Structuring partnerships or joint ventures

Proper preparation can significantly improve approval timelines and project execution.

Final Thoughts

The CMHC MLI Select program offers some of the most attractive financing terms available for multi-family real estate investment in Canada.

However, those benefits are designed for well-prepared and financially disciplined investors.

By understanding deposit requirements, liquidity expectations, and net worth thresholds, investors can position themselves strategically to access these opportunities.

Preparation is not just a requirement. It is a competitive advantage in one of the fastest-growing sectors of the Canadian real estate market.

Frequently Asked Questions for Investor Requirements

Q. What is the CMHC MLI Select Program?

The program is a mortgage insurance initiative that supports multi-unit residential properties with five or more units by providing enhanced financing terms for qualifying projects.

Q. How much deposit is required for an MLI Select investment?

Most projects require investors to provide approximately 5 to 10 percent of the total project cost as an accessible deposit.

Q. What liquidity is required for CMHC MLI Select investors?

Investors are typically required to maintain 10 percent of the total project cost in liquid assets as a contingency reserve.

Q. What net worth is needed to qualify?

Borrowers generally need a minimum net worth equal to about 25 percent of the project cost, though exact requirements may vary by lender and project structure.

Q. Why does CMHC require these financial standards?

These requirements reduce risk, ensure responsible development, and protect the long-term stability of insured multi-family financing.

Q. Can investors partner to meet qualification requirements?

Yes. Joint ventures and investment partnerships are commonly used to combine capital strength and meet qualification benchmarks.