A Detailed Guide to Requirements and Point Optimization

The CMHC MLI Select Program has significantly reshaped multifamily mortgage financing across Canada by linking improved loan terms to measurable social and environmental performance. For investors and developers, the program offers powerful financial advantages, including higher leverage and longer amortization periods.

However, qualifying for the program requires more than simply applying for mortgage insurance. Projects must meet strict financial standards while strategically earning points across several impact categories.

This guide explores both the foundational eligibility requirements and the strategies investors can use to maximize their MLI Select score.

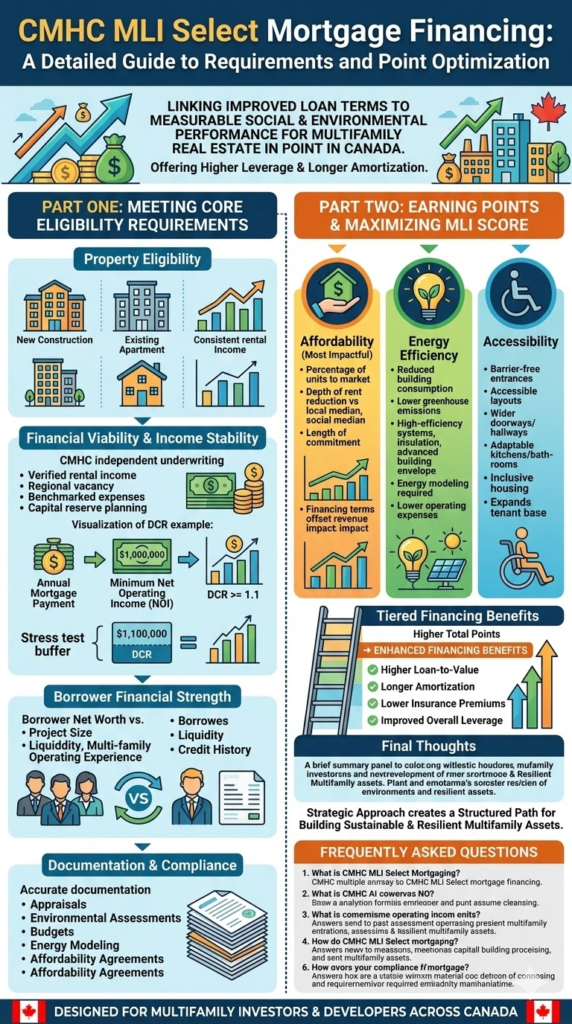

Part One: Meeting the Core Eligibility Requirements

Before a project can benefit from enhanced financing terms, it must satisfy several baseline requirements designed to ensure financial stability and responsible lending.

These requirements form the foundation of the program’s risk management framework administered by Canada Mortgage and Housing Corporation.

Before a project can benefit from enhanced financing terms, it must satisfy several baseline requirements designed to ensure financial stability and responsible lending.

These requirements form the foundation of the program’s risk management framework administered by Canada Mortgage and Housing Corporation.

Property Eligibility

MLI Select applies to multi unit residential rental properties that generate stable rental income.

Eligible property types generally include:

Purpose built apartment buildings

Existing stabilized multifamily rental properties

New construction rental developments

The property must meet minimum unit thresholds established by lenders and comply with CMHC guidelines for residential rental housing.

Projects that generate consistent rental income and demonstrate long term viability are typically the strongest candidates for approval.

Financial Viability and Income Stability

The most important requirement for approval is proof that the property can generate reliable cash flow over time.

CMHC conducts its own independent underwriting analysis rather than relying solely on borrower projections. This evaluation typically includes:

Reviewing rental income using verified market comparables

Applying regional vacancy assumptions

Benchmarking operating expenses against industry averages

Assessing long term capital reserve planning

A key metric used in this analysis is the debt coverage ratio requirement.

The program requires a minimum debt coverage ratio of 1.1, meaning the property must generate at least 110 percent of the income required to service the mortgage.

For example:

If annual mortgage payments equal one million dollars,

The property must generate at least one million one hundred thousand dollars in net operating income.

This financial buffer ensures that properties remain resilient even if market conditions change or operating costs increase.

Borrower Financial Strength

In addition to the property’s financial performance, borrower qualifications are also evaluated carefully.

Lenders and CMHC typically assess:

Borrower net worth relative to project size

Liquidity to cover deposits and potential contingencies

Experience operating or managing multifamily properties

Credit history and overall financial stability

Borrowers with a strong financial profile and relevant real estate experience generally face a smoother approval process.

Documentation and Compliance

Applicants must provide detailed documentation to support both financial projections and project characteristics.

Typical documentation includes:

Independent property appraisal reports

Environmental site assessments

Construction budgets and development timelines

Energy modeling studies, when applicable

Affordability agreements for qualifying units

Accuracy and transparency are essential during the submission process. If projections appear overly optimistic, CMHC may apply more conservative assumptions when evaluating the project.

Part Two: Earning Points to Improve Your MLI Score

Once baseline eligibility requirements are satisfied, the next objective is maximizing the project’s MLI Select score.

The scoring system determines the level of financing advantages available to the borrower.

Projects earn points across three primary categories:

Affordability

Energy efficiency

Accessibility

Each category contributes to the overall point total, which determines the financing tier the project can access.

Affordability

Affordability is one of the most impactful scoring categories within the program.

Points are awarded based on several factors, including:

The percentage of units offered below market rent

The depth of the rent reduction relative to local median rents

The length of time the affordability commitment is maintained

For example, offering a small number of reduced rent units for a short period will generate fewer points than offering deeper rent reductions over a longer time frame.

Although affordability commitments may reduce some potential rental revenue, improved financing terms such as longer amortization periods and higher leverage can often offset part of that impact.

Energy Efficiency

Energy efficiency improvements represent another major opportunity to earn points under the program.

CMHC evaluates how a property’s energy performance compares with baseline standards. Projects may earn points by:

Reducing overall building energy consumption

Lowering greenhouse gas emissions

Installing high efficiency heating and cooling systems

Improving insulation and window performance

Using advanced building envelope design

Energy modeling studies are typically required to demonstrate the projected performance improvements.

In addition to earning points, energy efficient buildings often benefit from lower operating expenses, which strengthens long term financial performance.

Accessibility

Accessibility is the third scoring category within the MLI Select framework.

Accessible design improves housing inclusivity while expanding the potential tenant base.

Points may be awarded for incorporating features such as:

Barrier free entrances and common areas

Accessible unit layouts

Wider doorways and hallways

Adaptable kitchens and bathrooms

As Canada’s population continues to age, accessible housing is expected to become increasingly important. Buildings that include these features are often better positioned for long term rental demand.

Tiered Financing Benefits

The total number of points achieved determines the financing benefits available to the borrower.

As projects move into higher scoring tiers, they may qualify for progressively stronger mortgage terms such as:

Higher loan to value ratios

Longer amortization periods

Lower insurance premiums

Improved overall financing leverage

This tiered system encourages investors to intentionally design projects that combine strong financial performance with positive community impact.

Final Thoughts

The CMHC MLI Select Program provides one of the most sophisticated financing frameworks available for multifamily real estate in Canada.

By linking improved mortgage terms with affordability, sustainability, and accessibility goals, the program encourages responsible development and long term housing stability.

For investors and developers who approach the process strategically, MLI Select offers far more than favorable financing. It creates a structured pathway for building sustainable, resilient multifamily assets.

Frequently Asked Questions for CMHC MLI Select Mortgage Financing

Q. What is the CMHC MLI Select Program?

The MLI Select program is a mortgage loan insurance program designed for multi unit residential rental housing in Canada. It rewards projects that contribute to affordability, energy efficiency, and accessibility with improved financing terms.

Q. What types of properties qualify for MLI Select financing?

Eligible properties typically include purpose built rental apartment buildings, stabilized multifamily properties, and new construction rental developments.

Q. What is the minimum debt coverage ratio required?

Projects must demonstrate a minimum debt coverage ratio of 1.1. This means net operating income must be at least 110 percent of annual mortgage payments.

Q. How are MLI Select points calculated?

Projects earn points across three categories affordability, energy efficiency, and accessibility. The total number of points determines the financing tier available to the borrower.

Q. Do energy efficiency improvements help qualify for better financing?

Yes. Projects that demonstrate measurable reductions in energy consumption may earn additional points, which can improve financing terms and reduce long term operating costs.

Q. Why is accessibility important for MLI Select projects?

Accessibility features expand housing options for a wider range of residents and support long term demographic trends such as an aging population.