For multifamily investors, mortgage financing is often the single largest factor determining whether a project succeeds or struggles. The CMHC MLI Select Program was designed to improve financing access while ensuring long-term housing stability. To truly understand its value, it is important to look closely at how the program works and how it evaluates mortgage risk.

What CMHC MLI Select Actually Is

CMHC MLI Select is a mortgage loan insurance program specifically created for multi-unit residential properties in Canada. It provides insurance to approved lenders, protecting them against loss in the event of borrower default.

Because the loan is insured by CMHC, the lender assumes less risk. This reduced risk allows lenders to offer borrowers more favorable mortgage terms than conventional uninsured multifamily financing.

However, this benefit is not automatic. The project must meet strict underwriting and performance standards before insurance is approved.

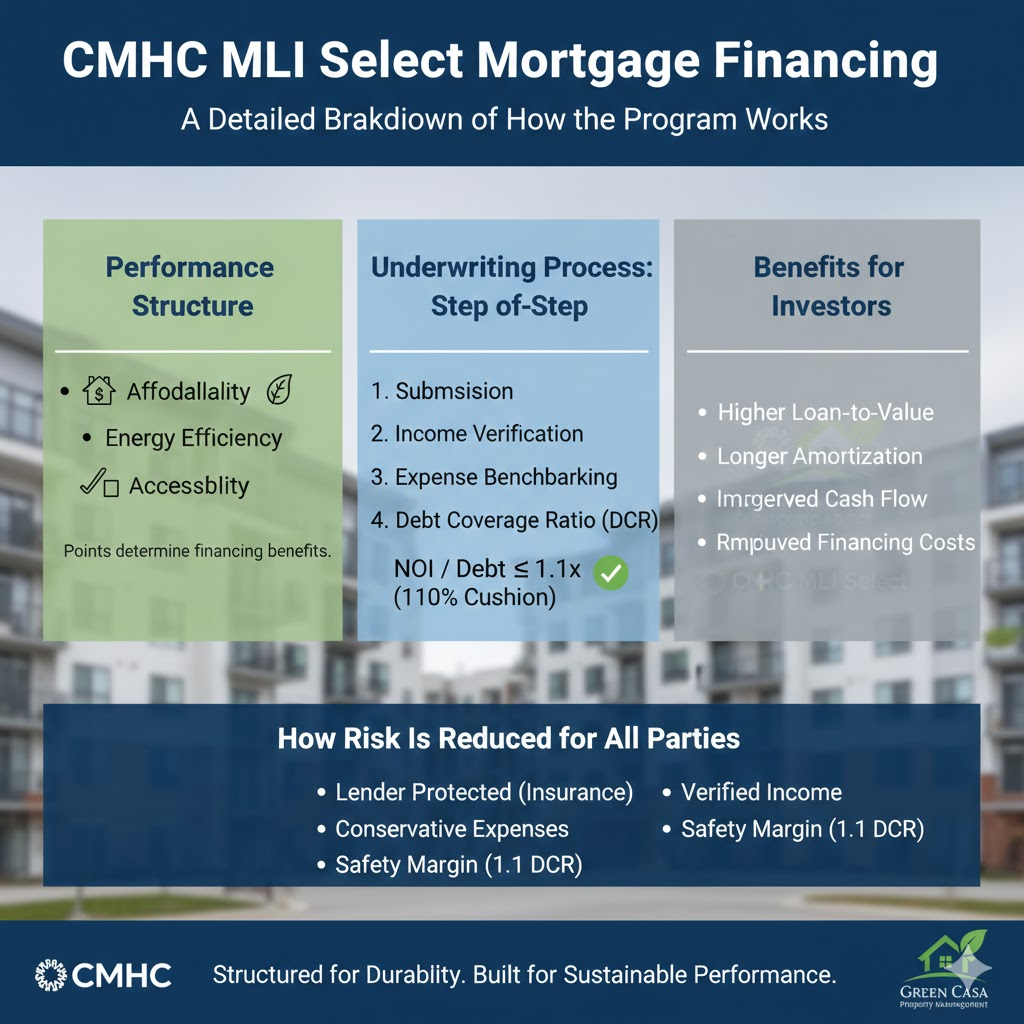

The Performance-Based Structure

Unlike traditional mortgage insurance programs that focus primarily on loan-to-value ratios, MLI Select incorporates a performance-based scoring model.

Projects earn points based on how well they address:

Affordability

Energy efficiency

Accessibility

Each category contains measurable benchmarks. The total points achieved determine the level of financing benefits available, including higher leverage and longer amortization periods.

This framework encourages responsible development while giving borrowers flexibility in how they qualify.

The Underwriting Process Step by Step

The mechanics of risk assessment are detailed and deliberate.

1. Borrower and Project Submission

The borrower works with an approved lender to submit a full financing package. This includes:

Detailed rent rolls or projected rental income

Operating expense breakdowns

Property appraisal

Environmental reports

Construction budgets, if applicable

Evidence of affordability or efficiency measures

The lender conducts its own credit and financial review before forwarding the file to CMHC.

2. Independent Income Verification

CMHC does not rely solely on borrower projections. It performs its own income analysis using regional rental benchmarks and comparable property data.

If projected rents exceed what the market realistically supports, CMHC will adjust them downward. This conservative approach prevents inflated revenue assumptions.

3. Expense Benchmarking

Operating expenses are evaluated against industry standards. Underestimating expenses is a common risk in multifamily underwriting. CMHC applies standardized expense ratios to ensure the property’s financial model reflects realistic operating costs.

This includes allowances for:

Property management

Maintenance and repairs

Utilities

Insurance

Replacement reserves

4. Debt Coverage Ratio Requirement

One of the most important safeguards is the debt coverage ratio requirement.

To qualify, the project must demonstrate that its projected net operating income equals at least 110 percent of projected annual debt payments. This creates a minimum 1.1 debt coverage ratio.

In practical terms, if annual mortgage payments total one million dollars, the property must generate at least one million one hundred thousand dollars in net operating income.

This ten percent cushion acts as a financial buffer, protecting both lender and borrower from short-term market fluctuations.

How Risk Is Reduced for All Parties

The program reduces mortgage risk in multiple layers:

The lender is protected through mortgage insurance.

Income projections are independently verified.

Expenses are benchmarked conservatively.

Debt coverage requirements create a safety margin.

Projects must align with long-term housing priorities.

This layered approach results in financing that is structured for durability rather than short-term gain.

Why This Matters for Investors

For borrowers, this rigorous process may seem demanding. However, it ultimately strengthens the investment.

Longer amortization periods improve monthly cash flow.

Higher leverage allows more efficient capital deployment.

Stable underwriting supports long-term refinancing opportunities.

CMHC MLI Select is not simply a cheaper mortgage option. It is a structured financing framework built on risk management and sustainable performance.