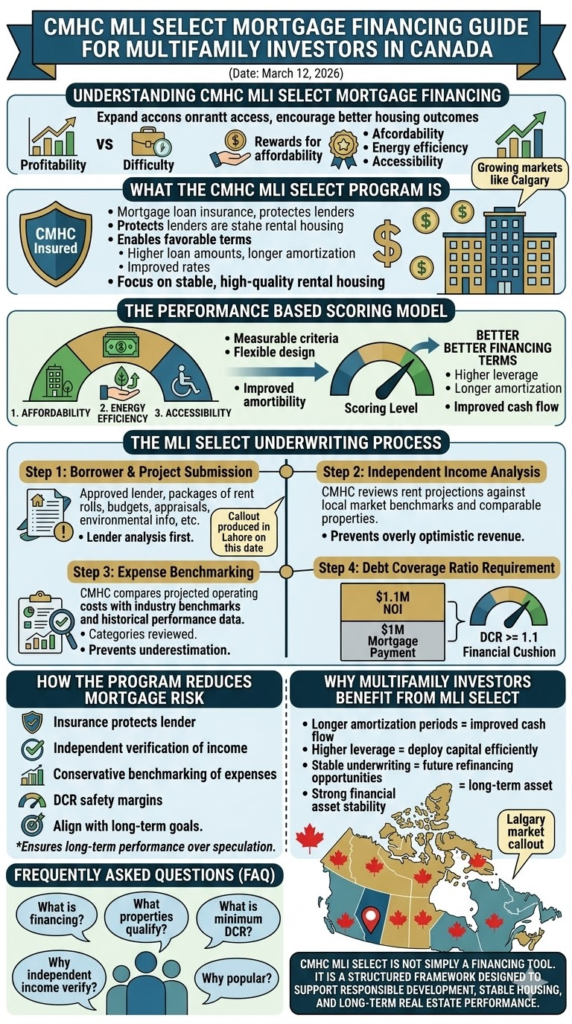

Understanding CMHC MLI Select Mortgage Financing

For multifamily investors, financing often determines whether a real estate project becomes profitable or financially difficult to sustain. In Canada, the CMHC MLI Select program has become one of the most important financing tools available for multi unit residential developments.

The program was designed to expand access to financing while encouraging better housing outcomes. It rewards projects that support affordability, energy efficiency, and accessibility while maintaining strong financial fundamentals.

For property owners and developers in growing markets such as Calgary, understanding how this financing structure works can significantly improve long term investment performance.

What the CMHC MLI Select Program Is

CMHC MLI Select is a mortgage loan insurance program designed specifically for multi unit residential properties across Canada.

The insurance protects lenders against financial loss if a borrower defaults on a mortgage loan. Because the loan carries this insurance protection, lenders are able to offer more favorable terms than traditional uninsured multifamily financing.

These advantages may include higher loan amounts, longer amortization periods, and improved interest rate options. However, borrowers must meet strict underwriting standards before the mortgage insurance is approved.

The program is designed not only to support financing but also to encourage the development of stable, high quality rental housing.

The Performance-Based Scoring Model

Unlike conventional mortgage insurance programs that focus mainly on loan to value ratios, the MLI Select program uses a performance based scoring framework.

Projects earn points based on how they address three major priorities.

Affordability

Energy efficiency

Accessibility

Each category includes measurable criteria. The more points a project earns, the more favorable the financing structure becomes.

For example, projects that achieve higher scores may qualify for higher leverage ratios and longer amortization periods. This can dramatically improve long term cash flow and investment stability.

The scoring model allows investors flexibility in how they design their projects while still aligning with national housing priorities.

The MLI Select Underwriting Process

The underwriting process for CMHC MLI Select financing is structured to ensure that projects remain financially viable over the long term.

Borrower and Project Submission

The process begins when the borrower works with an approved lender to submit a comprehensive financing package.

This package usually includes

Current rent rolls or projected rental income

Operating expense projections

Independent property appraisal

Environmental assessments

Construction budgets for the project, if it is a new development

Documentation showing affordability or energy efficiency features

The lender first performs its own credit and financial analysis before submitting the file to CMHC.

Independent Income Analysis

CMHC independently reviews the projected rental income for the property.

Rather than relying entirely on borrower projections, the agency compares expected rents with local market benchmarks and comparable rental properties.

If projected rents appear too high relative to the market, CMHC may adjust them downward to reflect realistic expectations. This conservative approach helps prevent overly optimistic revenue assumptions.

Expense Benchmarking

Operating expenses are also carefully evaluated.

In many real estate projections, expenses are underestimated. CMHC addresses this risk by comparing projected operating costs with industry benchmarks and historical performance data.

Expense categories typically reviewed include

Property management fees

Maintenance and repair costs

Utilities

Insurance expenses

Long term replacement reserves

By ensuring realistic expense assumptions, the program strengthens the financial reliability of the project.

Debt Coverage Ratio Requirement

One of the most important safeguards in the underwriting process is the debt coverage ratio requirement.

To qualify for CMHC MLI Select financing, the property must demonstrate that its projected net operating income equals at least 110 percent of its annual mortgage payments. This creates a minimum debt coverage ratio of 1.1.

For example, if a building has annual mortgage payments of one million dollars, the project must generate at least one million one hundred thousand dollars in net operating income.

This built in financial cushion helps protect both lenders and borrowers from short term market fluctuations.

How the Program Reduces Mortgage Risk

The CMHC MLI Select framework reduces mortgage risk through several layers of financial protection.

Mortgage insurance protects the lender from default losses

Income projections are independently verified

Operating expenses are benchmarked conservatively

Debt coverage ratios create financial safety margins

Projects must align with long term housing priorities

These safeguards help ensure that financing decisions are based on sustainable long term performance rather than short term speculation.

Why Multifamily Investors Benefit from MLI Select

For investors, the underwriting process may initially appear demanding. However, the long term advantages can be substantial.

Longer amortization periods can significantly improve monthly cash flow

Higher leverage allows investors to deploy capital more efficiently

Stable underwriting supports future refinancing opportunities

Strong financial structures improve long term asset stability

For multifamily investors in growing Canadian cities like Calgary, these advantages can make the difference between a good investment and a great one.

The CMHC MLI Select program is not simply a financing tool. It is a structured framework designed to support responsible development, stable housing, and long term real estate performance.

Frequently Asked Questions for CMHC MLI Select Mortgage Financing

Q. What is CMHC MLI Select financing?

CMHC MLI Select is a mortgage loan insurance program for multi unit residential properties in Canada. It provides lenders with insurance protection while rewarding projects that support affordability, energy efficiency, and accessibility.

Q. What types of properties qualify for MLI Select?

The program is designed for multi unit residential properties such as apartment buildings, purpose built rentals, and certain mixed use developments with residential components.

Q. What is the minimum debt coverage ratio for MLI Select?

Projects must demonstrate a minimum debt coverage ratio of 1.1, meaning net operating income must be at least 110 percent of annual mortgage payments.

Q. Why does CMHC verify rental income independently?

CMHC reviews rental projections using market benchmarks to ensure the financial model reflects realistic revenue expectations.

Q. Why is MLI Select popular with multifamily investors?

The program offers benefits such as higher leverage, longer amortization periods, and improved financing terms, which can significantly improve investment performance.