A Strategic Breakdown of Requirements and Scoring Mechanics

For multifamily investors across Canada, securing the right financing can determine whether a project achieves long term success or struggles with financial limitations. The CMHC MLI Select Program was created to reward projects that combine financial stability with broader housing goals such as affordability, sustainability, and accessibility.

The program operates on a straightforward principle. Projects that contribute positively to housing supply and long term community stability deserve stronger financing support.

However, achieving approval and unlocking the full benefits of the program requires more than simply meeting minimum standards. Successful applicants approach the process strategically, structuring their projects to maximize both financial eligibility and performance based scoring.

Understanding how the program evaluates risk and assigns points enables investors to position their projects more effectively.

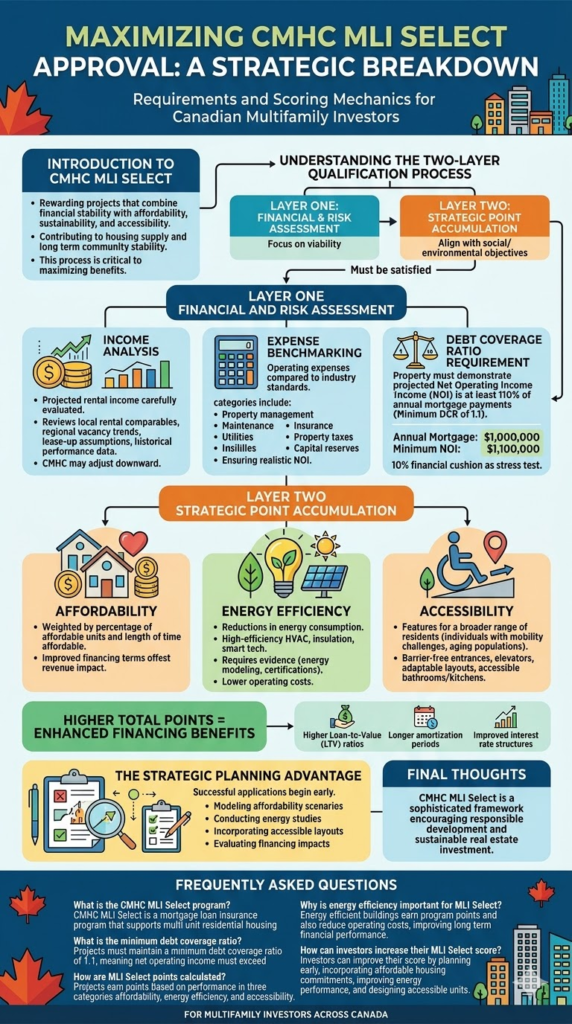

Understanding the Two-Layer Qualification Process

The MLI Select approval process can be understood as a two-layer system.

The first layer focuses on financial viability and risk management.

The second layer evaluates how well a project aligns with the program’s broader social and environmental objectives.

Only projects that satisfy both layers can access the enhanced financing terms available through the program.

This dual evaluation framework ensures that projects receiving favorable mortgage conditions are both financially stable and aligned with long term housing priorities.

Layer One Financial and Risk Assessment

Before performance scoring is even considered, Canada Mortgage and Housing Corporation conducts a detailed financial analysis to confirm that the property can sustain long term mortgage obligations.

The underwriting process is deliberately conservative. Its purpose is to prevent unrealistic projections and ensure the property remains financially resilient through different market conditions.

Income Analysis

Projected rental income is carefully evaluated using several sources of market data.

CMHC reviews

Local rental comparables

Regional vacancy trends

Lease up assumptions for newly constructed properties

Historical performance data for similar assets

If projected rents exceed realistic market expectations, CMHC may adjust them downward. This protects both lenders and borrowers from overly optimistic revenue assumptions that could jeopardize the financial stability of the property.

Expense Benchmarking

Operating expenses are another critical component of the risk evaluation process.

Many real estate projections underestimate expenses in order to produce stronger financial models. CMHC addresses this by benchmarking projected operating costs against industry standards and comparable properties.

Expense categories reviewed typically include

Property management costs

Maintenance and repair budgets

Utilities and building operations

Insurance premiums

Property taxes

Capital reserve allocations for future building improvements

By applying realistic cost assumptions, CMHC ensures that the projected net operating income accurately reflects the long term financial performance of the property.

Debt Coverage Ratio Requirement

One of the most important safeguards within the underwriting process is the debt coverage ratio threshold.

To qualify for the program, a property must demonstrate that its projected net operating income is at least 110 percent of its annual mortgage payments. This creates a minimum debt coverage ratio of 1.1.

In practical terms, if a property’s annual mortgage obligations total one million dollars, the building must generate at least one million one hundred thousand dollars in net operating income.

This ten percent financial cushion acts as a stress test, ensuring the property has sufficient revenue to withstand short term fluctuations in occupancy or operating costs.

Projects operating on extremely tight margins often struggle to meet this requirement.

Layer Two Strategic Point Accumulation

Once financial viability is confirmed, borrowers have the opportunity to enhance their financing terms by earning points within the MLI Select scoring system.

Projects earn points across three major categories

Affordability

Energy efficiency

Accessibility

The total number of points achieved determines the level of financing benefits available.

Higher point totals can unlock advantages such as

Higher loan to value ratios

Longer amortization periods

Improved interest rate structures

This framework encourages investors to incorporate meaningful design and operational improvements into their projects.

Affordability as a Long Term Commitment

Affordability is one of the most heavily weighted categories within the scoring system.

Points are awarded based on both the percentage of affordable units within a project and the length of time those units remain affordable.

For example, a property that designates a larger portion of its units as affordable and commits to maintaining those rents for a longer period will receive a higher score.

While affordability commitments may appear to limit revenue potential, improved financing terms can often offset this impact. Longer amortization periods and higher leverage can significantly improve monthly cash flow.

When structured strategically, affordability and financial performance can coexist effectively.

Energy Efficiency as an Operational Advantage

Energy performance improvements represent another powerful way to increase MLI Select scores.

Projects that demonstrate measurable reductions in energy consumption may qualify for higher point tiers within the program.

Examples of energy improvements include

High efficiency heating and cooling systems

Enhanced building insulation

Energy efficient windows and building envelopes

Smart building technologies that optimize energy usage

To receive points, projects must typically provide documented evidence such as energy modeling studies or performance certifications.

Beyond earning points, energy efficient buildings often experience lower operating costs, which can improve long term net operating income.

Accessibility and Long Term Market Demand

Accessibility is the third major scoring category within the MLI Select framework.

Accessible design ensures that residential buildings can accommodate a broader range of residents, including individuals with mobility challenges or aging populations.

Features that may contribute to accessibility scoring include

Barrier free building entrances

Elevators and accessible circulation paths

Adaptable unit layouts

Accessible bathrooms and kitchens

As demographic trends shift and populations age, accessible housing is expected to become increasingly important.

Projects that incorporate inclusive design not only earn program points but also expand their potential tenant base.

The Strategic Planning Advantage

The most successful MLI Select applications begin long before financing documents are submitted.

Investors who plan strategically during the acquisition or development stage are often able to maximize their project’s score with relatively modest adjustments.

Key planning steps may include

Modeling different affordability scenarios

Conducting energy performance studies early in the design phase

Incorporating accessible layouts within building plans

Evaluating how incremental improvements impact financing benefits

In many cases, relatively small design or operational changes can significantly increase the total MLI Select score. This can translate into improved financing structures that strengthen long term investment performance.

Final Thoughts

The CMHC MLI Select Program represents one of the most sophisticated multifamily financing frameworks available in Canada.

Rather than simply providing mortgage insurance, the program encourages responsible development, financial stability, and long term housing quality.

Meeting baseline financial requirements ensures eligibility. Strategic planning within the scoring framework unlocks the program’s most valuable financing advantages.

For multifamily investors willing to approach the process thoughtfully, MLI Select offers far more than improved mortgage terms. It provides a structured path toward sustainable real estate investment and long term portfolio growth.

Frequently Asked Questions for Debt Coverage Ratio Requirement

Q. What is the CMHC MLI Select program?

The CMHC MLI Select program is a mortgage loan insurance program that supports multi unit residential housing projects that promote affordability, sustainability, and accessibility.

Q. What is the minimum debt coverage ratio required?

Projects must maintain a minimum debt coverage ratio of 1.1, meaning net operating income must exceed mortgage obligations by at least ten percent.

Q. How are MLI Select points calculated?

Projects earn points based on performance in three categories: affordability, energy efficiency, and accessibility.

Q. Why is energy efficiency important for MLI Select?

Energy efficient buildings earn program points and also reduce operating costs, improving long term financial performance.

Q. How can investors increase their MLI Select score?

Investors can improve their score by planning early, incorporating affordable housing commitments, improving energy performance, and designing accessible units.