The CMHC MLI Select Program has quickly become one of the most attractive financing tools for multi-unit residential investors in Canada. With longer amortizations, reduced insurance premiums, and incentives for affordable and energy-efficient housing, the program offers exceptional leverage. However, access to these benefits comes with clear financial expectations.

If you’re considering applying, understanding the qualifying criteria is essential before moving forward.

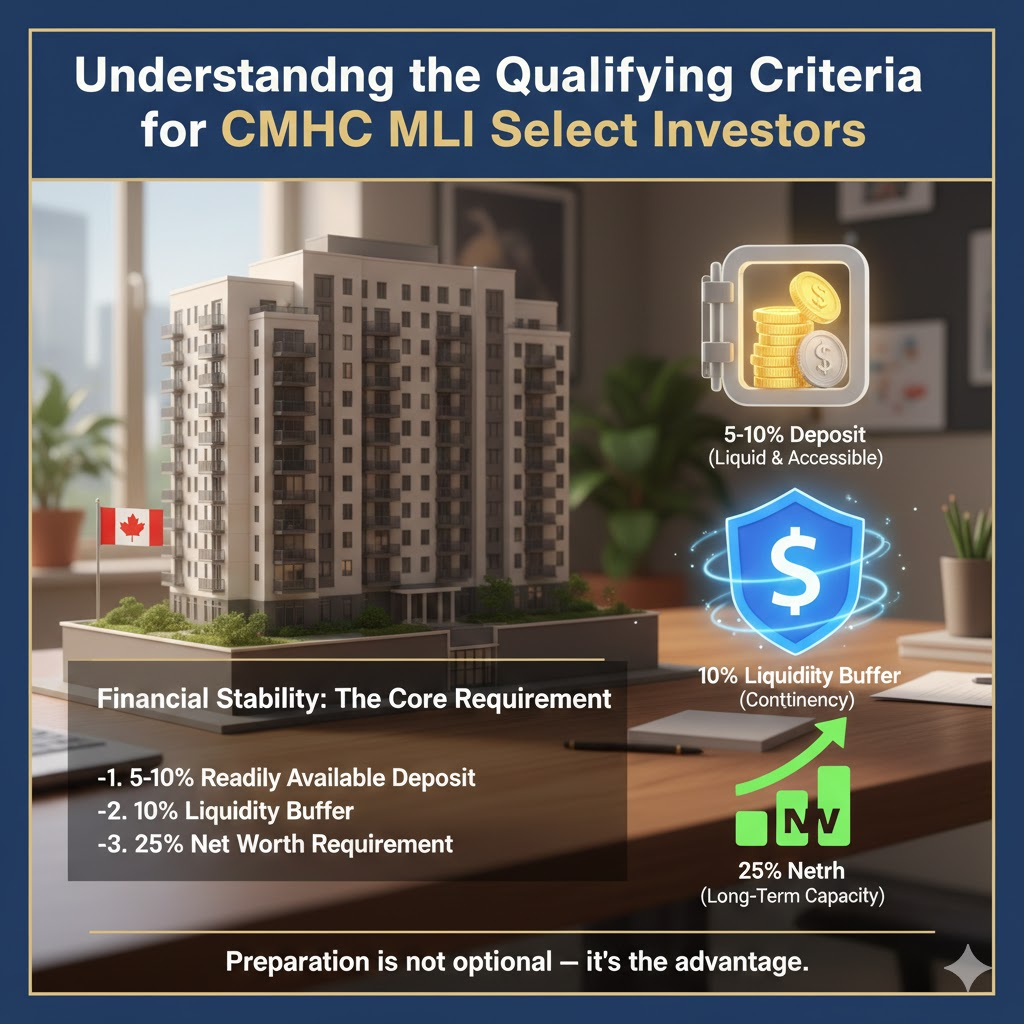

Financial Stability: The Core Requirement

CMHC is not only financing real estate, but it’s also financing borrowers. As a result, an investor’s financial strength plays a central role in approval decisions. To qualify, purchasers must demonstrate that they can support the project through acquisition, stabilization, and long-term ownership.

This is measured through three primary benchmarks: deposit availability, liquidity, and net worth.

1. Readily Available Deposit (5–10% of Project Cost)

Investors are required to have 5–10% of the total project cost available as a deposit, depending on the deal structure and lender requirements.

This capital must be:

- Liquid (cash or near-cash equivalents)

- Accessible without selling long-term assets

- Verifiable through bank or investment statements

The deposit demonstrates commitment and reduces early-stage risk for both the lender and CMHC.

2. Liquidity Buffer: 10% Contingency Requirement

Beyond the deposit, CMHC requires investors to maintain an additional 10% of the total project cost in liquid assets.

This contingency buffer exists for a reason:

- Construction delays

- Cost overruns

- Lease-up risks

- Unexpected operational expenses

Liquid assets may include:

- Cash

- High-interest savings accounts

- Marketable securities (subject to lender approval)

This requirement reassures CMHC that the project can survive unforeseen challenges without financial distress.

3. Net Worth Requirement: Minimum 25% of Project Cost

Investors must also demonstrate a personal net worth equal to at least 25% of the total project cost.

Net worth includes:

- Real estate equity

- Investment portfolios

- Business ownership

- Cash and savings

- Other tangible assets

This benchmark ensures the borrower has sufficient long-term financial capacity to support the loan, especially during market shifts or economic downturns.

Why CMHC Sets These Standards

CMHC’s underwriting is conservative by design. These criteria:

- Protect public-backed financing

- Encourage responsible development

- Reduce default risk

- Support long-term housing stability

For qualified investors, these standards also act as a filter, keeping competition lower and deal quality higher.

Final Thoughts

The CMHC MLI Select Program rewards well-prepared investors. If you can demonstrate adequate liquidity, a strong net worth, and disciplined capital planning, the program can unlock some of the most attractive financing terms in the Canadian multi-family market.

Preparation is not optional; it’s an advantage.